There has been much speculation regarding the demand for super fast broadband speeds, which for the sake of this post, I define as 30 Mbps and above. Many industry observers say broadband carriers must upgrade their networks and offer these and faster speeds to remain competitive. After some quick analysis, I’m not so sure, at least for the time being.

There has been much speculation regarding the demand for super fast broadband speeds, which for the sake of this post, I define as 30 Mbps and above. Many industry observers say broadband carriers must upgrade their networks and offer these and faster speeds to remain competitive. After some quick analysis, I’m not so sure, at least for the time being.

These same observers point to an advantage that DOCSIS 3.0 enabled cable companies have over telephone companies who offer DSL. All major cable MSOs offer faster broadband speeds than the DSL offers from their telco competitors, thanks to their use of DOCSIS 3.0. AT&T probably best represents this telco competitor, since almost all of their broadband service is DSL delivered. Even U-Verse is DSL, albeit a hybrid FTTN DSL offer. AT&T faces competition from all of the major cable MSOs, and by all accounts, offers a slower broadband offer, much slower in some cases.

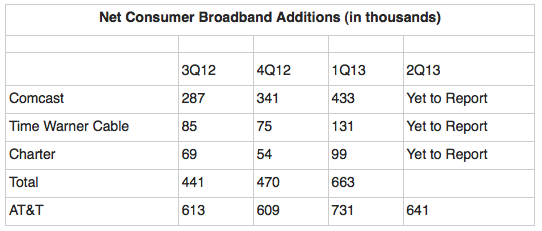

Yet, if you take a look at broadband subscriber metrics over the past year, AT&T is outperforming all of the cable MSOs, by a long shot. AT&T is first to report 2Q13 numbers, during which they added 641K net broadband additions. If 2Q13 compares in any way to the previous three quarters, AT&T is crushing their faster cable competitors. For the past three quarters, AT&T has more broadband net adds than three of the top five cable MSOs of Comcast, Time Warner Cable, and Charter, combined (see table below).

Most, if not all, of those net adds are U-Verse broadband, considering AT&T (and Verizon) lose considerable legacy DSL subscribers every quarter. AT&T’s best U-Verse offer is 24 Mbps, for now anyway. That compares with DOCSIS 3.0 offers from their cable competitors that can range from 50 Mbps to 305 Mbps, on the high end. If higher speed broadband tiers are so important, how is it AT&T is adding more broadband subscribers than three of the top five cable MSOs combined?

This is not exhaustive research by any stretch. It’s simply a quick analysis of quarterly numbers. There are factors that certainly come into play here that have not been considered, like sales promotions, bundling, etc. It’s also a singular moment in time, of three to four quarters. Maybe it’s cyclical, considering Comcast was beating both AT&T and Verizon for a period.

But for this moment in time, one could draw the conclusion that super fast broadband is not as an important as we may think it is.