The U.S. mobile market is entering a new evolutionary phase as consumer adoption of mobile and wireless devices and services nears, or has reached, saturation, according to Strategy Analytics. With the base of new customers shrinking, U.S. wireless network operators are now focusing on promoting “always on” connectivity, moving customers to smartphones and 4G LTE service, and finding ways to monetize data use, the market research company summarizes in a press release.

The U.S. mobile market is entering a new evolutionary phase as consumer adoption of mobile and wireless devices and services nears, or has reached, saturation, according to Strategy Analytics. With the base of new customers shrinking, U.S. wireless network operators are now focusing on promoting “always on” connectivity, moving customers to smartphones and 4G LTE service, and finding ways to monetize data use, the market research company summarizes in a press release.

Mobile Subscriber Forecast

Even with growth in new subscribers slowing, nearly 100 million wireless subscribers will be added to the U.S. market by 2020, which will bring market penetration to 128 percent, according to Strategy Analytics’ “U.S. Wireless Market Outlook 2015-2020.” That includes new connections from consumer electronics (CE) devices but excludes fast-growing M2M (machine-to-machine) connections.

Turning to revenue, Strategy Analytics forecasts the U.S. wireless market will grow 0.2% to reach $197 billion in 2020. That would be up just slightly from 2015’s $195 billion. Rising prepaid service revenue and that for data service will fuel growth, increasing 5.7 percent and 3.3 percent, respectively.

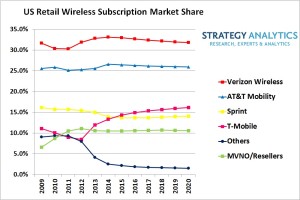

When it comes to market players and competition, Strategy Analytics sees Verizon Wireless and AT&T continuing as the dominant wireless carriers as they diversify their revenue streams. That said, the research firm expects T-Mobile USA and Sprint to gain ground.

With T-Mobile USA having passed Sprint as the third-largest U.S. wireless carrier in mid-2015 in terms of subscribers, the market research company does foresee industry rankings changing among the top four. Wireless wholesalers, MVNOs and resellers will gain a slightly higher percentage of net adds over the next couple of years, according to a second new market research report, “US Wireless Outlook: Can T-Mobile and Sprint Disrupt AT&T and Verizon Wireless?.”

“As the US market focuses on the next stage of its evolution – from voice to text to data and now to constant connectivity and what you do with it — competition for market share and retention of subscribers takes center stage,” Susan Welsh de Grimaldo, director for Straegy Analytics’ Wireless Operator Strategies, was quoted as saying.

“Neck-and-neck numbers three and four – T-Mobile USA with its pro-consumer ‘Un-carrier’ strategy and straggler Sprint that has shown great strides in network performance – are focused on network efforts to reach LTE network parity with the top two and [on] market offers aimed to grow share, yet need to also address higher churn levels and margins.”

Added Phil Kendall, Wireless Operator Strategies’ executive director: “The top two carriers – Verizon Wireless and AT&T – share strategies as ‘defenders’ of market leadership to find growth by diversifying revenue base, building platforms, engaging the broader ecosystem, and developing multiscreen video offerings.

“Yet there is perhaps more divergence in their strategies now than in recent years. Other players add to the dynamic market place, with Google now entered on to the scene as an MVNO and DISH having amassed more spectrum but not revealing strategy. MVNOs have been on an upswing, with Wi-Fi first and target segment approaches.”